Deduction Limitations for Self-Directed IRAs (Traditional)

When Congress passed the Employee Retirement Income Security Act of 1974 (ERISA) – the law that created the traditional Self-Directed IRA we still use today, lawmakers recognized that we as a country had a vested interest in encouraging workers to save for their own retirement security. And so they did so by granting a tax incentive: Contribute to these accounts, thereby committing to keep your money in the IRA until retirement age or pay a 10 percent early withdrawal penalty (to keep people honest!) and the IRS will let you take an immediate tax deduction for the contribution. For most people, they would not be taxed on money they weren’t consuming. By essentially deferring consumption and using the IRA, they can invest what would have been taxed, as well. And as a sweetener, the IRS let investors and savors defer income taxes on dividends and interest, as well.

When Congress passed the Employee Retirement Income Security Act of 1974 (ERISA) – the law that created the traditional Self-Directed IRA we still use today, lawmakers recognized that we as a country had a vested interest in encouraging workers to save for their own retirement security. And so they did so by granting a tax incentive: Contribute to these accounts, thereby committing to keep your money in the IRA until retirement age or pay a 10 percent early withdrawal penalty (to keep people honest!) and the IRS will let you take an immediate tax deduction for the contribution. For most people, they would not be taxed on money they weren’t consuming. By essentially deferring consumption and using the IRA, they can invest what would have been taxed, as well. And as a sweetener, the IRS let investors and savors defer income taxes on dividends and interest, as well.

Note: This article focuses specifically on issues related to the traditional IRA – whether self-directed or not. If you want information on the Roth IRA, that’s an upcoming blog post, so stay tuned!

Now, that tax deferral used to be a bigger deal than it is today, at today’s substantially reduced dividend levels and interest rates (remember the 70s and 12-13 percent mortgages?!). But the tax deferral still has significant value. And for active traders, it has even more – IRAs allow investors to avoid paying capital gains taxes on their trades.

But the Congress did not intend that tax break to go on forever. They designed the IRA so that the Treasury would, eventually, get that tax revenue it gave up when you made the contribution.

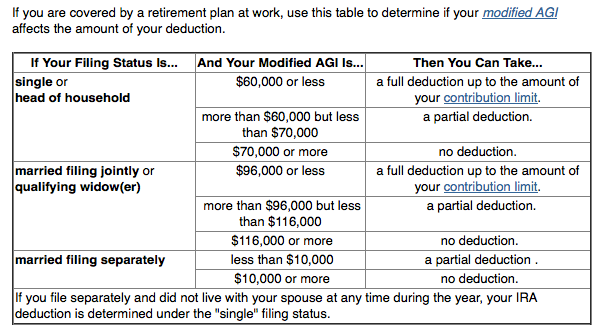

Congress also did not want just anybody taking the tax break. Instead, they wanted to focus the benefits of the IRA for people who were earning middle to upper-middle class incomes – especially if they do not have a retirement plan at work. And so Congress limited the ability of higher-earning workers and those with access to workplace plans to deduct contributions. (These workers may still make non-deductible contributions, up to $5,500 in 2014, but the current year tax breaks are still mostly reserved for those with more moderate incomes and those who do not have a workplace retirement plan.

Here are the tables for 2014, right from the IRS:

Normally, you must make IRA contributions with earned income. However, if you qualify, you can also make contributions for your spouse, even if your spouse is not working outside the home and therefore does not have earned income.

Applicability to Self-Directed IRAs

If you have a Self-Directed IRA, the income limitations on the allowable contribution are exactly the same. However, many Self-Directed IRA owners choose to boost their effective investments within their IRAs by using leverage: That is, borrowed money.

Generally, you can borrow up to about two times the assets within a Self-Directed IRA, or a little less, provided you do so on a non-recourse basis. In other words, the most you will be able to borrow is two dollars per dollar of collateral within the IRA. For example, the most companies that specialize in IRA lending will lend is 65 percent of an investment – you would have to start out with 35 percent down – even for real estate loans.

You cannot pledge anything outside the IRA as collateral for a loan to your IRA, and your IRA cannot borrow from you, from your spouse, your descendants or ascendants, nor any entity any of these people control.

By borrowing money and using leverage in this way, however, you can effectively nearly triple the amount of capital at work in your Self-Directed IRA.

For example: You start with a $70,000 balance in your Self-Directed IRA. You identify a property selling for about $200,000 and you would like to acquire it using your IRA. Your $70,000 that you have available down is sufficient for a 35 percent down payment. The lender puts up the remaining $130,000, so your IRA effectively has a $200,000 asset generating income and capital gains.

Caution: It’s not all gravy. The lender charges interest, of course. But more directly, the IRS only allows you to defer taxes on income attributable to your own contribution! Not on the income resulting from the money you borrowed!

Under unrelated debt-financed income tax rules, you will still have to pay income tax on 65 percent of the income your property generates.

This is something that catches some Self-Directed IRA investors unaware, but it’s important to know about, because you will need to have the cash ready from somewhere to pay the income tax!

This can be a problem. But with the right kind of planning well ahead of time, you can minimize or eliminate its effects. For example: Had an IRA owner in this situation not used an IRA for the transaction, but kept the assets in a self-directed solo 401(k) plan instead, the unrelated debt income tax would not have applied!

This is an example of the value of using an administrator with specific expertise in self-directed retirement accounts: Asset location can make a big difference when it comes to self-directed retirement accounts!

For more information on IRA deduction limits, see IRS Publication 590, Individual Retirement Arrangements. Or better yet, give us a call at 866-7500-IRA (472), or visit us at https://americanira.com. One of our experts will be able to boil things down for you quickly and help you apply it to your own situation, in conjunction with your own financial advisor.

Image by: presentermedia.com